- Colorado Business Registration

Colorado Business Registration

$99 - Order Now

By Jonathan Feniak, Esq., MBA

Asset Protection

Protect your home, savings, and lifestyle.

Low Fees

We charge $99 to form your company and act as the registered agent for the first year. In future years our registered agent service is $59.

Private Ownership

Colorado does not require LLC and Corporation owners be listed. Use our name instead.

New Tax Laws

Save more on taxes than you spend on formation.

Simplicity

Everything is done within 24 hours.

Professionalism

Increases trust compared to a Sole-Proprietorship.

Registering a Business

Your passion may be painting houses, building houses, or walking dogs. Eventually, the question becomes whether you should operate as a sole proprietor or register a business in Colorado. This page is meant to help answer that question. We provide guides designed to make forming and operating your Colorado company easy. We cover the differences between forming a Colorado LLC, Sole-Proprietorship and Corporations.

After choosing an entity, learn how to obtain your Employer Identification Number (EIN), file your periodic report, set up a virtual office, open a bank account, what a registered agent is, how get a free phone number and more. Keep scrolling to learn more.

What is a Sole Proprietorship?

A business is a sole proprietorship when the person is the business. Sole proprietorships are owned by one person and have no legal requirements to start or operate. Many people who start a small business opt for this default structure or have this structure without even knowing it because they don't chose another structure. They require no extra paperwork, but they can require the owner to pay more in taxes and they offer no asset protection.

The major negatives of a sole proprietorship are that they may cause the owner to pay more in taxes and that they offer the owner no protection for the owner's personal assets.

Unlimited Liability:

A sole proprietorship has unlimited liability and the owner is personally responsible for all debt of the business. You as the owner are also liable if someone sues the business because the business is you! If someone wins a lawsuit against the owner, the owner can be forced to sell personal belongings to pay legal judgments. This is known as unlimited liability and is a major negative of operating a business as a sole proprietorship.

Higher Taxes:

A sole proprietor pays the same taxes as a wage earner. This means there is no way to take advantage of the new tax code directed at small businesses and paying too much in earned income taxes.

Not Professional:

Doing business in your personal name is less professional than operating as a business. Clients and vendors will know you have not taken the extra step to register with the state, that you cannot have any partners, and that your business can only grow so large. Having a business entity shows your customers that you are there for the long term and this is more than a side project.

Discloses Private Info:

Forming an LLC provides you with greater privacy. Colorado's Secretary of State does not list owners or managers of entities on its website, so the owner of a business can keep their personal information private. Contrast this to a sole-prop where your name appears everywhere and people know your home address. Learn more about LLC privacy here.

Rather than spending a lot on insurance, and hoping to not be sued, you may form an LLC or a Corporation for additional protection. Each has better tax treatment which more than cover the minimal cost of incorporating with us.

Order NowLLC Fees

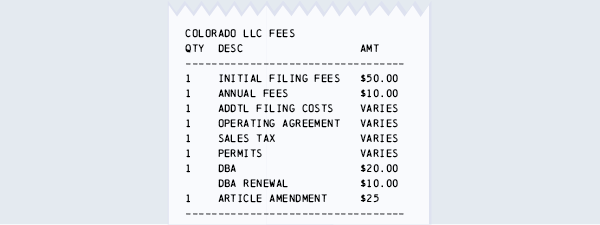

Colorado LLCs have minimal required fees to be maintained. There is a periodic report, also known as an annual report, that must be filed with the Secretary of State. This report is used to confirm your address and other relevant information for the company. The report and maintaining a registered agent is everything that's required to keep your company in good standing with the Secretary. Find a full page on Colorado LLC fee schedule for various corporate actions here.

LLC Taxes

A Colorado LLC can be taxed in one of four ways: disregarded entity, partnership, S Corporation or as a C-Corp. By default if there's one owner your LLC will be taxed as a disregarded entity. If there are two or more members, then "partnership" taxation is the default classification. An S-Corp or C-Corp requires a separate filing with the IRS. This flexibility provides LLCs a tax advantage compared to Corporations. To learn more about pass through taxes, double taxation and more, please visit our page on Colorado LLC taxes.

LLC Operating Agreement

Every limited liability company should have an operating agreement. This agreement makes clear the responsibilities and rights of the owners and managers. An operating agreement is a contract that all parties sign to show their understanding. It delineates ownership percentages and required contributions, among other important items. Our LLC formation service includes an agreement free of charge. It's important to note single member LLCs should have an agreement too because it shows courts that the LLC is taken seriously and should be given the protection of limited liability.

Order NowSingle Member LLC

A single-member LLC is simply a company that has one owner. The owner of an LLC is called a member, and so any limited liability company with one owner is called a single-member LLC. They are taxed as disregarded entities by default: the same as a sole-proprietorship. They do not generally give the owners the same level of asset protection as multi-member LLCs.

LLC vs Corporations

Formal corporate structures, such as LLCs and Corporations, have some very attractive points and are similar in several ways. They exist as their own entities and are their own "individuals" in the eyes of the law.

Similarities

- Both LLCs and Corporations conduct business with the rights and responsibilities of a person. They are legally separate from their owners, and therefore responsible for their own debts.

- This separation is what provides owners with personal protection from company liabilities. Both entities also protect the owners from the negligent acts of other owners. Neither sole proprietorships nor partnerships offer this.

- Since a company is its own entity, its life span is not linked to any person and it can live forever. This is what it means for an entity to be of perpetual duration.

Differences

- Corporations may find it easier to raise capital. Multiple share classes offer greater versatility which investors tend to favor. The downside is corporations pay more in taxes and have greater burdens when it comes to corporate governance.

- Corporations are subject to double taxation which means that both the corporation's income is taxed and the income given to its owners through dividends is taxed as part of the owner's personal income. The only exception to double taxation is an S Corporation where owners report their share of the company's income as part of their personal income.

- Corporations have more rigid operating structures and titles. For example, Corporations must have a President and a Board of Directors. Usually, the managers are not the owners in a corporation.

- Most companies are now formed as limited liability companies because they offer the best of both worlds: a corporation's limited liability and the tax benefits of both partnerships and sole proprietorships.

Frequently Asked Limited Liability Questions

A sole proprietorship is when the person is the business. If there is little chance or incurring liability or you are ok with taking on the liability yourself, then a sole-proprietorship may be an ok way for you to operate your business. They offer no asset protection, so all your personal assets will be at risk.

If there are multiple owners you can't operate as a sole-proprietorship, but you can operate as a partnership. If you want anything more than a 50/50 split of the business you will need an agreement. For LLCs this is called an operating agreement and for Corporations these are called the bylaws.

The simplest forms of each of they documents treat each owner equally. However, in some situations you may want more complex arrangements in which certain owners have more rights, get a larger share of profits, or have more power. For example, perhaps you wish for silent partners who only contribute money, but cannot make decisions or sign on the company’s behalf. In such a case an LLC is a good fit.

On the other hand, perhaps you want multiple classes of ownership. Some of whom have no voting rights, others who receive a guaranteed return before others, and another who does not share in profits until the fifth year. In this case, a Corporation is generally a better fit. Their bylaws and articles allow for much more complex arrangements. However, with such complexity comes additional cost. Leading us to our next question…

The final factor is the amount of money available for the entity structuring process. Individuals with almost no budget opt for sole-proprietorships, but those with a modest budget often opt for an LLC. With our help you can form your LLC and provide yourself with asset protection, tax benefits, and ownership flexibility. Those that have money set aside, or more complex needs, can invest in forming a Corporation.

A corporation will be preferred in situations where a complex shareholder agreement is required. Otherwise, a limited liability company can achieve asset protection and tax benefits at a lower costs with reduced corporate formalities. Unless you have received specific legal or accounting advice otherwise, it is generally preferable to form an llc.

We will file everything correctly the first time. We will put our information into the public record rather than yours. We are fast and can form your company in less than 24 hours. We also have a number of resource articles on getting a free business phone, opening a bank account, obtaining your EIN, along with registering foreign corporations and LLC.

Colorado LLC Checklist

When conducting business in Colorado, there are number of rules and regulations to pay attention to. These requirements come at the local, state, and federal level and must be followed in order to avoid penalties and maintain good standing with the state. Here, we’ve provided a checklist of things to consider when starting your business in Colorado. Due to the variety of business-types and industries, this list is not comprehensive. However, it should serve as a good starting point for most businesses.

Starting a Business in Colorado

The following is an overview of the steps you will take to start your business in Colorado:

- Choose a name and conduct a search to ensure availability.

- Select the appropriate business entity type.

- Register with the Colorado Secretary of State.

- Obtain an Employer Identification Number.

- Open a bank account for your business.

- Register with the Colorado Department of Revenue if you need to collect sales tax.

- Obtain all necessary permits or licenses.

* Choosing a Business Name

While it may seem simple in theory, choosing a business name should be given considerable thought and planning. Ideally, you will choose a name that is memorable and easy to associate with your given industry, service, or product. Additionally, pick a name that gives a positive impression and conveys an appropriate image of your company to the public.

* Choose a Business Entity Type

The next important step in your business formation is deciding which type of entity best fits your personal and business needs. The different entity options are sole proprietorship, partnership, limited liability company, or corporation. Sole proprietorships are one-person businesses. If you operate a sole-proprietorship there is not a legal distinction between your business assets and your personal assets. Partnerships are treated the same as sole proprietorships, with the owners having unlimited liability. The only distinction is that a partnership operates with two or more individuals. Limited liability companies, or LLCs, are recognized as legally separate entities and will protect the owner's personal assets from business liability. Corporations are entirely separate legal entities often formed to run larger businesses. Corporations offer limited liability protection to its shareholders.

* Register with the CO Secretary of State

In order to properly register your business in the state of Colorado, you must file articles of incorporation or organization with the Secretary of State. To file your articles, visit the Secretary of State webpage here: http://www.sos.state.co.us/biz/FileDoc.do. The filing fee and official registration form varies between business entity type:

- Sole Proprietorship: $20, Statement of Trade Name of an Individual

- Partnership: $25, Statement of Trade Name

- LLC: $50, Articles of Organization

- Corporation: $50, Articles of Incorporation

* Obtain an EIN

Next, you should obtain an Employer Identification Number, also known as a Federal Tax ID Number. This is a unique number the IRS assigns to your business for tax purposes. It is sometimes referred to a social security number for your business. Additionally, your EIN can be used to file taxes and open a bank account, among other things. You can obtaining an EIN by completing an online application with the IRS or through our EIN service.

* Open a Business Bank Account

It is important to open a separate bank account for your business for a number of reasons. Among them is the need to separate your business assets from your personal assets for both legal considerations and good accounting practices. Once you have opened an account, your bank can provide you with debit and credit cards.

* Register with the CO Department of Revenue

Once you have formed your business, it is important that you also register with the Department of Revenue if you are selling goods because you will be required to collect sales tax. If you are registering as a sole proprietorship, partnership, or LLC, you will need to file the Colorado Form 104. If you are registering as a corporation, then you will need to file the Colorado Form 112. Calculating taxes for your business can be a complex process. Any mistakes can lead to penalties and negative marks against your business. If you want to ensure this process is handled correctly, enlist the services of an expert accountant.

* Permits & Licenses

Depending on the nature of your business, additional permits or licenses may be required. Once you have registered your business with the Colorado Secretary of State and obtained an EIN from the IRS, check into which permits and licenses apply to your business. Two good resources for this information are The Division of Professions and Occupations and the Colorado Small Business Navigator.

* Forming a Colorado LLC

If you would like assistance with forming your Colorado LLC, consider using our LLC formation service. Our expert guidance can ensure that your LLC complies with all Colorado state requirements, while also protecting your personal information.

Order Now